Every so often, contemporary crises pique public interest in historical matters. There are few better examples of this than the current fascination with redlining.

In 2018, African American families had, on average, just one-tenth of the wealth of their white counterparts. While discrimination in education and employment have intensified this gap, home values and the continuation of racially discriminatory lending practices, experts believe, have helped exacerbate this disparity.

In 2014, Ta-Nehisi Coates revisited the case for reparations not by looking at slavery, but rather at the historical legacy of Jim Crow segregation and discriminatory housing policies. Coates knew that African Americans, who had to live in redlined communities and suffered housing discrimination as a fact of life, were still victims of this history. Coates, who later brought these matters before Congress in 2019, was a major figure in the regeneration of popular redlining remembrance.

Richard Rothstein's The Color of Law (2017), which outlined the legacy of housing discrimination and redlining, also revived widespread interest in New Deal housing policies – and their relationship to contemporary residential segregation.

While we have Rothstein and Coates to thank for helping to put redlining back on the map of public consciousness, the popular narrative that has taken hold may obscure longer patterns of housing injustice, stretching from emancipation through urban renewal and beyond.

In terms of redlining, the typical story goes:

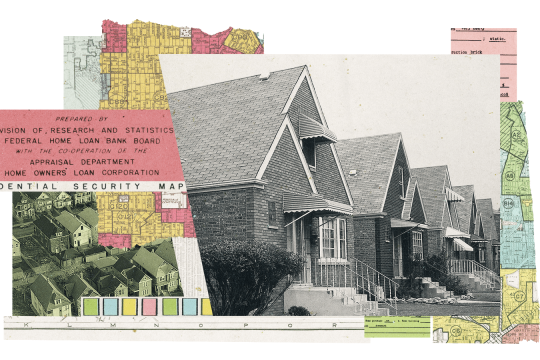

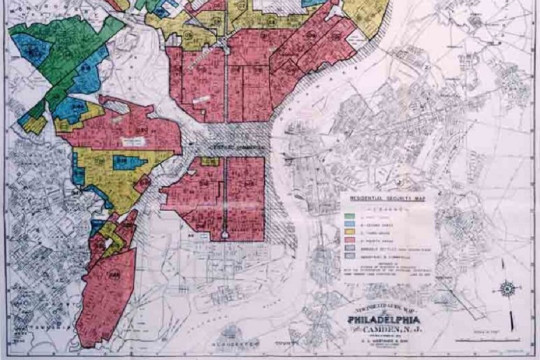

After the Great Depression, homeownership became essential to American wealth-building. The New Deal coalition, which passed the Home Owners’ Loan Act in 1933, set aside millions of dollars for home loans, helping to build the culture of American homeownership.

By the mid-1930s, public and private actors had taken to assessing financial risk in housing markets with recourse to race. Assessors graded neighborhoods using a color-coded mapping system — African American communities, regardless of their socioeconomic standing, were almost always given red distinctions. In deeming certain neighborhoods hazardous or dangerous, red distinctions devalued property. This methodology of racial risk assessment all but confirmed the already prevalent belief that black people brought down property values.

In time, lenders’ systematic financial withdrawal from African American communities gave rise to predictable outcomes, simultaneously creating white suburbs and Black inner-cities.

But what does this story leave out? Redlining, some scholars contend, has become a “narrative crutch” that obscures a much longer history of housing discrimination. Redlining didn’t create systemic racism in American housing patterns – it sanctioned it.

Before the Great Depression, exclusionary zoning laws relegated African Americans communities to the most undesirable and dangerous sections of America’s cities.

By the 1950s, efforts to modernize American cities had racial implications too. Slum clearance and urban renewal, subsidized by federal dollars, were often openly referred to as “Negro Removal.” Between 1949 and 1974, African American neighborhoods (and the property and culture within them) were systematically wiped out. African Americans rarely got fair market value for their homes.

In the mid-20th century, urban planners and highway engineers designed one of the world’s most advanced freeway systems. They did so with little to no consideration for how highways might impact cities and the people within them—especially those with few resources or political clout. The proximity of Black communities to America’s downtowns meant that freeway systems, which often cut through the core of urban areas, decimated entire Black communities, either gutting them completely or cutting them in half—all in the name of suburban access to the city.

Meanwhile, these massive swaths of asphalt allowed whites to move into suburbs by the tens of millions. Suburbanization was one of the largest migrations of human beings in recorded history, aided and abetted by federal largesse. The political implications of this migration continue to shape American politics.

Well into the 1960s, federal officials refused to insure homes in integrated neighborhoods. If Black families could afford to buy into white neighborhoods, the Federal Housing Authority often refused to insure future mortgages even to whites in that neighborhood— integration would, officials argued, lead to violence, and violence heightened financial risk.

Restrictive racial covenants in housing deeds–provisions in contracts that limited what homeowners’ could and could not do with property–often precluded white homeowners from selling property to racial minorities. While the Supreme Court held that these covenants were unenforceable in a 1948 case known as Shelley v. Kraemer, they weren’t outlawed until the Fair Housing Act, 20 years later.

Between the 1940s and early 1970s, policymakers placed public housing facilities in already-devalued Black enclaves, compressing millions of people into racially segregated public housing facilities. Many of these spaces came to be characterized by profound and collective disappointment. They were also populated, in some cases, by the very African Americans that failed to get fair market value for their homes after they’d been decimated by urban renewal.

Projects, as they came to be known, eventually dotted the landscape of Black communities across America. The poverty that became synonymous with life in public housing still haunts many of America’s cities with sizable minority populations.

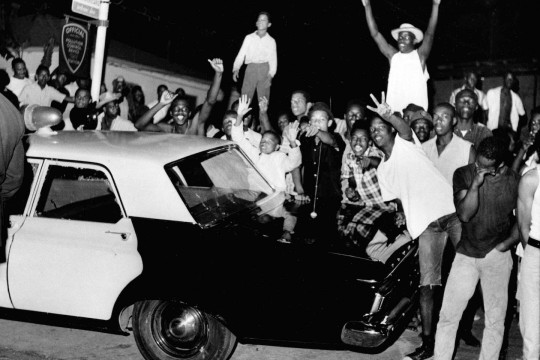

By the 1970s, African American neighborhoods were not just associated with low property values, but also with crime. Although tensions existed between Black people and police long before the long, hot summers of the late 1960s, open hostility between police forces and America’s urban black communities reached fever pitch in 1968. A half century before the massive protests of 2020, the over-policing Black communities was a central focus of the Civil Rights Movement.

The story of housing discrimination did not end there. Between the 1970s and 1990s, private investors and lending agencies flooded Black communities with subprime and reverse mortgages, sinking them even deeper into financial disrepair. Keeanga-Yamahtta Taylor has described this process as “predatory inclusion,” demonstrating how the very mortgage practices that led to the Great Recession had been taking place in Black communities as far back as the 1970s. Nonprofit organizations have, in many cities, supervised the resulting Black poverty, investing in and perpetuating the “eds and meds” strategy of urban renewal.

What does all of this mean?

It means that African Americans weren’t only denied a fair shot at homeownership and the generational wealth it often engenders; predatory interests very purposefully exploited the poverty created by that legacy of exclusion.

If the story of African Americans after the Civil War is, in some ways, an immigrant story (people migrating from the mostly rural south to northern and western cities), this tale belies the upward mobility that supposedly undergirds the American Dream. And while those who remained in rural, mostly southern areas endured their own version of land discrimination, many Black migrants found little relief in the North, Midwest, and West. Some have, in fact, returned south.

The history of redlining and the other mechanisms of housing discrimination also bely the narrative of the Civil Rights Movement as a story of triumph. The rights revolution of the 1960s (i.e., the Fair Housing Act of 1968) did little to mitigate housing injustice. This is a larger problem in the story of the rights revolution of the 1960s. Washington failed to follow up policies with the types of enforcement mechanisms that might have prevented backlash.

It wasn’t merely the federal government that segregated America. The real estate industry, private lenders, city planners, and even institutions of higher education also helped reinforce the biases that characterize housing discrimination. Vulnerable communities still feel the impacts of this profitable disinvestment in vast and far-reaching ways.

The perpetuation of racist residential patterns far exceeds the reach of government actors. Public and private actors are, in many ways, equally responsible for the spaces we do and do not inhabit to this day.

The long history of social and economic disinvestment may not have been inevitable, but it is still with us. Redlining is an essential component of understanding this history, but we can no longer rely on it alone to explain the continuity of urban inequality.